Pinterest Q3 2024: Why Is the Stock Price Falling Despite Strong Performance?

One stock that has been on my mind for over six months is Pinterest. PINS has struggled to deliver positive returns this year. In fact, year-to-date (YTD), it has dropped by a little over 20%, while the S&P 500 has gained nearly 25% in the same period. This makes me wonder: is Pinterest undervalued or overvalued?

Currently, the stock is trading at just above $28, which is about 65% below its all-time high (ATH) in February 2021 and 35% below its recent peak in June 2024.

Q3 2024 Financial Highlights

Despite the stock's price performance, the data in the following text shows that Pinterest is having one of its best quarters in history.

- Q3 revenue grew 18% year over year to $898 million

- Global Monthly Active Users “MAU” increased 11% YoY to record high 537 million

- Net income margin increased to 3% in Q3 2024 it was 1% in Q3 2023.

Given these results, it's no surprise that Pinterest's CEO, Bill Ready, is very pleased and describes the company as: “We delivered another strong quarter with users reaching another all-time high of 537 million and revenue growth at 18%. Our AI investments are driving results by powering better personalised experiences and greater performance for advertisers, with our lower-funnel ad tools being the fastest-growing part of our business. Advertisers are increasingly relying on Pinterest to engage our growing audience who see us as a great place to find inspiration, curate and shop.”

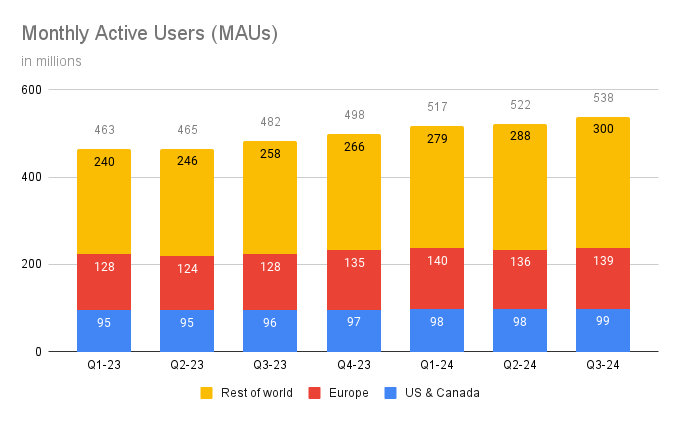

Monthly Active Users (MAUs) and Average Revenue Per User (ARPU)

One of the most important metrics for social media platforms is monthly and daily active users. For Pinterest, there are a few interesting insights on this topic.

Quarter over quarter, Pinterest has been increasing its Monthly Active Users (MAUs), with this quarter showing an 11% growth. The most significant part of this increase, according to many Pinterest investors, is the growth in the US and Canada. This is particularly important because it directly impacts the average revenue per user (ARPU), which we’ll discuss later.

While Pinterest is gradually growing its user base in Europe, this region has historically been a bit more challenging. Still, it’s encouraging to see the overall trend moving in a positive direction.

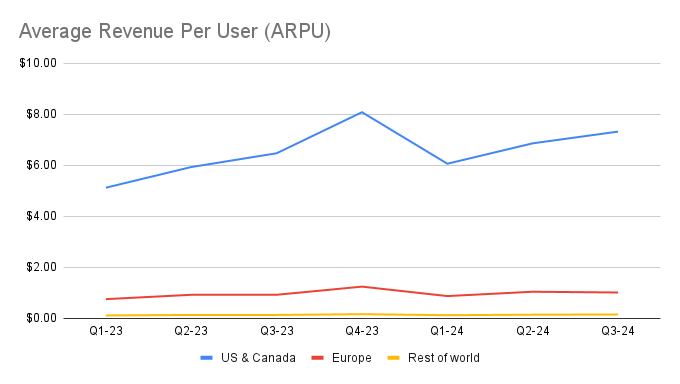

I find it even more interesting to look at revenue per user across different regions. This quarter, the average revenue per user (ARPU) in the US and Canada is $7.31, while in Europe it’s about $1, and in the rest of the world, just $0.14.

This highlights a significant difference: gaining 1 million new users in the US or Canada is far more impactful from a revenue perspective than in Europe or other regions. In fact, a user in the North America is over seven times more profitable than a European user and more than 50 times more profitable than one from the rest of the world.

For marketers, this is crucial information because they prefer to target audiences with higher spending power. While average revenues are slowly increasing in Europe (+10%) and the rest of the world (+18%), they still lag far behind the North American market.

Why stock price is decreasing?

After considering all of this, the real question is: why is the stock price decreasing? It's always tricky to pinpoint the reason, especially when the reports are so positive. The only downside I can see for this stock is their forecast for Q4.

“For Q4 2024, we expect revenue to be in the range of $1,125 million to $1,145 million, representing 15-17% growth year over year. We expect Q4 2024 Non-GAAP operating expenses* to be in the range of $495 million to $510 million, representing 11-14% growth year over year. Please note that our operating expense guidance does not include cost of revenue.”

From the guidance I copied from their report, it's clear that the relative growth next quarter is slightly smaller compared to what we saw previously. Typically, Q4 is a strong quarter for Pinterest due to the holiday season, when users spend more than at any other time of the year. This is reflected in the ARPU for Q4 2023.

However, I don’t expect major surprises in revenue, as Pinterest has been fairly transparent and on point with their guidance in its recent quarters.

With all this in mind, I believe Pinterest is undervalued, and I plan to increase my position over the next few weeks. My target price for the stock is between $50 and $72. I’ll reassess this decision in the upcoming quarters.